How to Use a 529 Plan for Your Child’s Future

Many parents want to give their children a strong start in life. They think about good schools, safe homes, healthy routines, and opportunities that may open doors later. One area that often creates both hope and stress is the rising cost of education.

College tuition, trade school programs, books, housing, and training expenses can feel intimidating, especially for families already managing mortgages, rent, groceries, insurance, and retirement savings. Many parents wonder how they are supposed to prepare for the future while also handling the present.

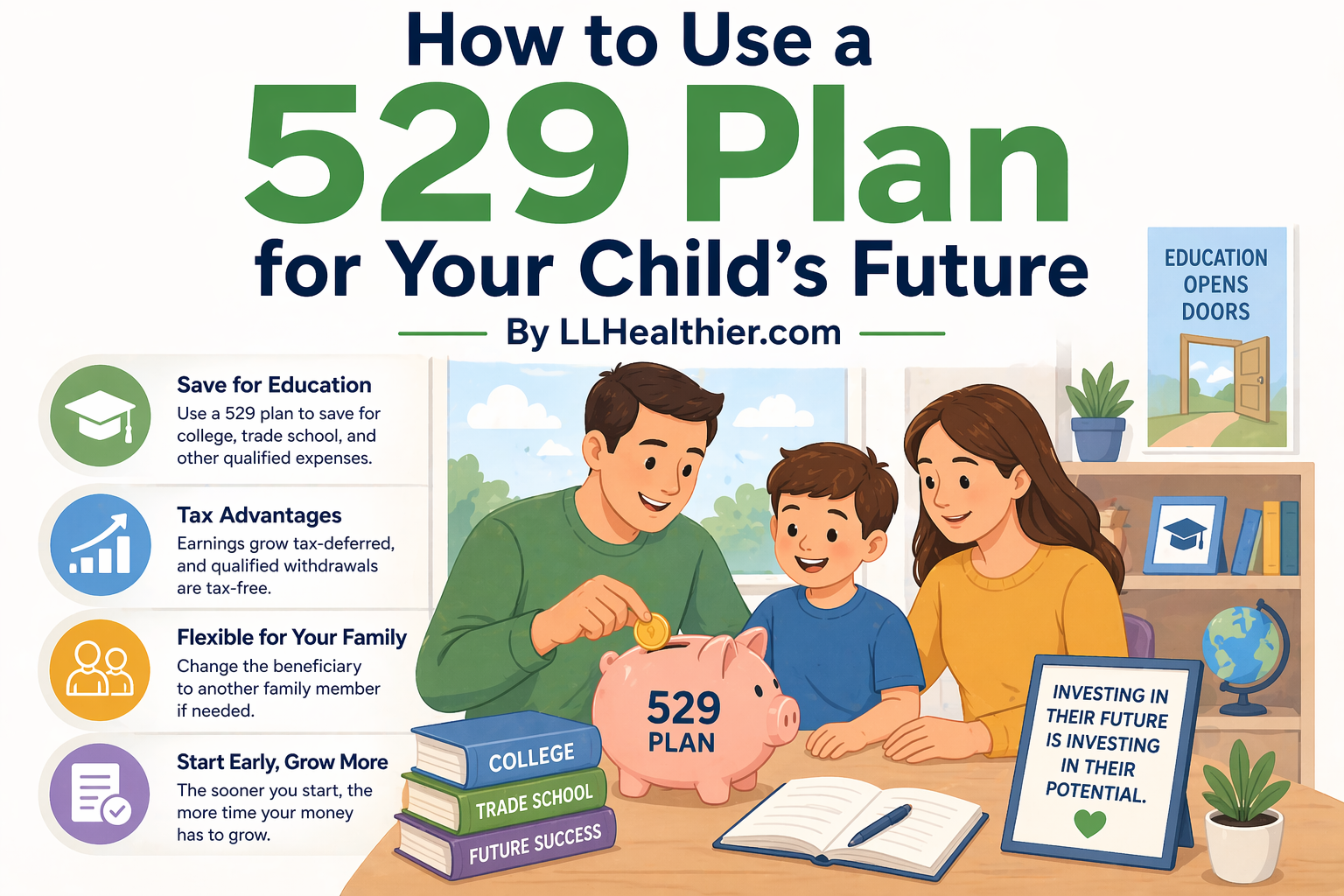

A 529 plan can be a helpful tool for many families. It offers tax advantages designed to encourage education savings, and when used thoughtfully, it can become part of a long-term strategy for helping a child pursue future goals.

The best part is that you do not need to be wealthy to use one. Many accounts begin with modest monthly contributions and grow over time through consistency.

What a 529 Plan Is

A 529 plan is a tax-advantaged savings account created to help families save for qualified education expenses. These plans are generally sponsored by states, though you are not always limited to using the plan from the state where you live.

Money placed into a 529 plan can be invested, which means it has the potential to grow over time depending on market performance and the investments selected. Earnings grow tax-deferred, and qualified withdrawals are generally tax-free when used for eligible education expenses.

That combination can make a meaningful difference over many years.

Think of a 529 plan as a dedicated education tool rather than a general savings account.

Why Families Consider a 529 Plan

Education costs have increased significantly over time. Even families who expect scholarships or in-state tuition often realize that expenses can still be substantial.

Beyond tuition, students may face fees, housing costs, meal plans, books, computers, transportation, and other related expenses.

A 529 plan can help reduce the future need for student loans, preserve family cash flow during college years, and create flexibility when opportunities arise.

It can also bring peace of mind. Many parents feel better knowing they are steadily preparing rather than hoping to figure everything out later.

Starting Early Matters

One of the strongest advantages of a 529 plan is time.

Money contributed early has more opportunity to grow through compounding. This means earnings may generate their own earnings over time. Even relatively small contributions made consistently can become meaningful over eighteen years.

For example, a family that starts when a child is a toddler often has a very different experience than a family trying to save aggressively during the final two years of high school.

That does not mean it is too late if your child is older. It simply means earlier usually helps.

Starting now is often better than waiting for a perfect future moment.

You Do Not Need Large Contributions

Some parents avoid opening a 529 plan because they assume they need thousands of dollars upfront.

That belief keeps many families from benefiting.

Many plans allow small initial deposits and automatic monthly contributions. Fifty dollars a month, one hundred dollars a month, or occasional larger gifts can add up over time.

Consistency often matters more than dramatic one-time deposits.

A modest monthly habit can become a substantial future resource, especially when started early and maintained steadily.

Choosing a State Plan

Every state’s 529 plan has its own investment options, fees, rules, and potential tax benefits. Some states offer residents a state tax deduction or credit for contributions to their in-state plan.

Other states have strong plans with low fees and broad investment options that attract families nationwide.

This means it can be wise to compare choices rather than assume the local plan is automatically best. At the same time, state tax benefits may tilt the decision in favor of your home state plan.

Review current plan details carefully or speak with a financial professional for personalized guidance.

Understanding Investment Choices

Most 529 plans allow you to choose among several investment approaches.

One common option is an age-based portfolio. These portfolios usually begin with more growth-oriented investments when the child is young, then gradually shift toward more conservative investments as college approaches.

Many busy parents appreciate this because it adjusts automatically over time.

Other plans allow custom selections among stock funds, bond funds, or blended portfolios.

The right fit depends on time horizon, risk tolerance, and overall financial picture.

What Expenses a 529 Plan Can Cover

529 plans are most commonly associated with college, but their use can be broader than many people realize.

Qualified expenses may include tuition and certain fees at eligible colleges, universities, vocational schools, and other approved institutions. Depending on circumstances and current law, room and board, books, supplies, and required equipment may also qualify.

Some plans may also be used for certain K-12 tuition expenses, apprenticeship programs, or student loan repayment limits under current rules.

Because laws can change, always verify current guidelines before taking withdrawals.

College Is Not the Only Future

Many families worry that if their child does not attend a traditional four-year college, the money will be wasted.

That concern is understandable, but it is often overstated.

Trade schools, technical programs, community colleges, and many career training paths may qualify if they meet eligible requirements. This matters because success comes through many routes, not one.

A child interested in welding, nursing, aviation maintenance, coding, cosmetology, or other practical careers may still benefit greatly from education savings.

What If One Child Does Not Use It

Life does not always follow the script parents imagine.

A child may receive scholarships, join the military, choose a lower-cost school, start a business, or decide on a different path.

In many cases, the beneficiary of a 529 plan can be changed to another eligible family member. This could include siblings and, in some circumstances, others within the family.

That flexibility can be valuable for households with multiple children or changing needs.

Scholarships and the 529 Plan

If your child receives scholarships, that is usually good news, even if it changes how much of the 529 balance is needed.

Families sometimes worry they will be penalized for saving.

Rules may allow certain withdrawals related to scholarships, though tax treatment can vary depending on circumstances. The key point is that receiving a scholarship does not automatically make the account a mistake.

In many cases, remaining funds can still be redirected or used strategically.

Avoiding Common Mistakes

One common mistake is prioritizing college savings while neglecting retirement savings entirely.

Parents can borrow for college more easily than for retirement. Children may have options such as scholarships, work, lower-cost schools, or loans. Retirees do not have the same flexibility.

Another mistake is waiting too long because the perfect amount feels impossible.

Progress usually begins with imperfect starts.

A third mistake is keeping all education savings in cash for many years, which may reduce growth potential after inflation.

Balance matters.

How Grandparents Can Help

Grandparents often want to support future education but may not know the best route.

A 529 plan can be an organized way to contribute birthday gifts, holiday money, or larger family contributions toward a child’s future.

Some families create gifting traditions where relatives contribute to the 529 instead of buying excessive toys or short-lived items.

This can create a meaningful multigenerational benefit.

It also gives family members a sense of participating in the child’s future opportunities.

Building a Practical Family Strategy

For many households, the best approach is not choosing between all goals. It is balancing goals.

That may mean contributing enough to receive any employer retirement match, maintaining an emergency fund, paying down harmful debt, and also making regular 529 contributions.

Some seasons of life allow larger contributions. Other seasons require smaller ones.

The habit matters.

Even pausing temporarily during hardship does not erase prior progress.

Talking to Your Child About It

As children grow older, it can be helpful to discuss education costs and savings openly in age-appropriate ways.

Knowing money has been set aside may encourage gratitude and motivation. It can also open conversations about choosing schools wisely, understanding value, and avoiding unnecessary debt.

This should not create pressure to follow one path.

Instead, frame the savings as support for learning and future growth.

What If You Started Late

Many parents feel regret when they discover 529 plans after years have passed.

Please do not let regret stop action.

Even a few years of saving can help with books, first-year expenses, community college costs, certification programs, or reducing total borrowing.

Late is not ideal, but late is often better than never.

Forward motion still counts.

Emotional Benefits Beyond Dollars

Money decisions are not purely mathematical.

For many parents, saving in a 529 plan represents care, intention, and hope. It reflects the desire to create options for a child later in life.

That emotional benefit matters too.

You may not be able to guarantee outcomes, but you can create opportunities.

When a 529 Plan May Not Be First Priority

There are seasons when a 529 plan should not be the immediate focus.

If you have no emergency fund, high-interest credit card debt, unstable housing, or no retirement savings at all, those issues may deserve earlier attention.

Financial planning is about sequence as much as strategy.

Helping your child includes protecting the whole household, not only one account.

A 529 plan can be a smart and flexible way to save for your child’s future education. It offers potential tax advantages, long-term growth opportunity, and the ability to prepare gradually over time.

You do not need a perfect income or a huge lump sum to begin. Small, steady contributions can build meaningful results.

Start early if you can. Start now if you cannot. Stay balanced with other financial priorities. Review options carefully and adjust as life changes.

The greatest gift is not only money set aside. It is creating future choices for the child you love.

Found this article interesting? Bookmark it to read again later.

Then, share it for others to read. 🌎

Thank you!

Post Comment