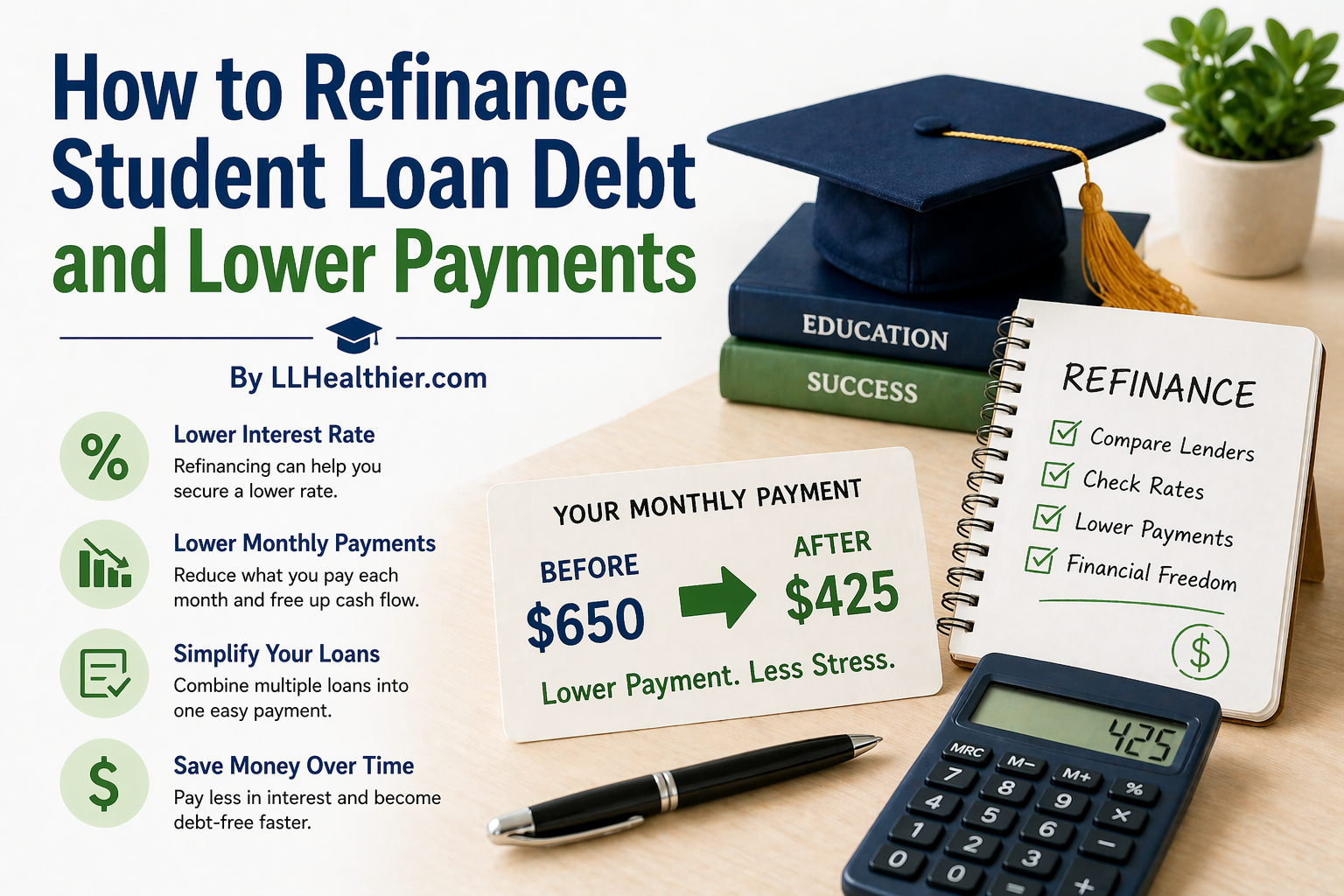

How to Refinance Student Loan Debt and Lower Payments

Student loan debt can feel like a long shadow over adult life. For many Americans, monthly payments compete with rent, groceries, childcare, saving for retirement, and trying to build a stable future. Even borrowers with steady jobs may feel stuck when payments consume too much of their income. The good news is that refinancing can sometimes create relief by lowering payments or reducing the total cost of the debt.

Refinancing means replacing one or more existing student loans with a new loan through a private lender. The new loan typically comes with a new interest rate, a new repayment term, and a new monthly payment. For the right borrower, refinancing can simplify finances and free up room in the monthly budget. For others, it may not be the best move, especially when federal loan protections would be lost.

Understanding how refinancing works can help you make a smart decision rather than an emotional one. The goal is not simply to chase the lowest advertised rate. The real goal is choosing a repayment structure that supports your long-term financial health.

What Refinancing Actually Changes

When you refinance, the new lender pays off your old student loans and issues you a brand-new loan. From that point forward, you make payments to the new lender under the new terms. This can apply to private student loans, federal student loans, or a mix of both depending on the lender.

The most common reason people refinance is to secure a lower interest rate. A lower rate may reduce the monthly payment, shorten the time needed to repay the loan, or lower total interest costs over the life of the debt. Some borrowers also refinance to combine multiple loans into one simpler payment.

This process can be useful, but it is not magic. It works best when the new terms are clearly better than the old ones.

When Refinancing May Make Sense

Refinancing often works best for borrowers with stable income, solid credit, and a history of on-time payments. Lenders reward lower-risk borrowers with better rates. If your credit score has improved since you first borrowed, refinancing may be more attractive now than it was years ago.

It may also make sense if your current loans have high interest rates. Private student loans taken out during college sometimes carry rates that feel painful later. Replacing a high-rate loan with a lower-rate loan can save meaningful money over time.

Borrowers who simply want a more manageable payment may also benefit by extending the loan term. This can lower the monthly bill, though it may increase total interest paid.

When Refinancing May Not Be Ideal

Refinancing federal student loans requires caution. Once federal loans are refinanced into a private loan, federal protections are usually lost. That can include income-driven repayment plans, generous deferment options, hardship protections, and certain forgiveness programs.

For borrowers working toward Public Service Loan Forgiveness or relying on federal flexibility, refinancing may be a costly mistake. A lower rate today may not outweigh benefits you give up tomorrow.

If your income is unstable or your emergency savings is weak, keeping federal protections may provide valuable peace of mind.

How Lower Payments Happen

Many people focus only on interest rates, but lower payments can happen in two primary ways. The first is securing a lower rate while keeping a similar term. This can reduce the payment and total interest cost at the same time.

The second is extending the repayment term. For example, moving from a seven-year schedule to a fifteen-year schedule can lower the monthly bill significantly. The tradeoff is usually paying more interest over many additional years.

This is why the cheapest monthly payment is not always the cheapest overall choice.

Check Your Credit Before Applying

Credit score plays a major role in refinance offers. Lenders often look at score, income, debt-to-income ratio, employment stability, and payment history. Stronger applicants generally receive better rates.

Before applying, review your credit reports for errors and pay down high credit card balances if possible. Even small improvements can help. Avoid missing any payments leading up to an application.

Think of credit as part of your negotiation power. Stronger numbers often create better options.

Compare Multiple Lenders

One of the biggest mistakes borrowers make is accepting the first offer. Different lenders may price the same borrower very differently. Shopping around can reveal meaningful differences in rates, fees, repayment terms, and customer service.

Many lenders allow prequalification with a soft credit inquiry. This can let you compare likely offers without harming your score. Pay attention to both fixed and variable rate options.

A little comparison shopping can save thousands over time.

Fixed Rate vs Variable Rate

A fixed interest rate stays the same for the life of the loan. This creates predictability, which many borrowers value. Your payment remains easier to budget because the rate does not rise with market changes.

A variable rate can start lower, but it may increase over time. If rates rise significantly, monthly payments can become uncomfortable. Some borrowers with aggressive payoff plans choose variable rates, but they come with more uncertainty.

For many average households, predictable payments create less stress.

Consider the Loan Term Carefully

Shorter terms usually mean higher monthly payments but lower total interest costs. Longer terms often reduce monthly pressure while increasing the amount paid overall. Neither choice is automatically right or wrong.

If cash flow is tight, a longer term may provide breathing room. If income is strong and other debts are manageable, a shorter term may help eliminate the loan faster.

The right term supports both math and real life.

Use a Cosigner if Helpful

Borrowers with limited credit history or weaker scores may receive better offers with a qualified cosigner. A parent, spouse, or trusted family member with strong credit can sometimes improve approval odds and rates.

However, cosigning is serious. If payments are missed, the cosigner may be affected financially and on their credit report. This should be approached with transparency and caution.

A cosigner can help, but the responsibility remains real for everyone involved.

Fees and Fine Print Matter

Many refinance loans do not charge origination fees, but terms still deserve careful review. Read for late fees, autopay discounts, hardship options, release of cosigner terms, and whether there are prepayment penalties.

You want flexibility in case life changes. A low rate loses appeal if the lender becomes difficult during hardship.

Price matters, but policy matters too.

Steps to Refinance Smoothly

Start by gathering your current loan balances, interest rates, monthly payments, and servicer details. Know what you owe before shopping. Then compare offers from multiple lenders and review the true monthly payment and long-term cost.

Once you choose a lender, complete the application and provide requested documents such as pay stubs or tax information. Continue making payments on your old loans until the refinance is fully completed and confirmed.

Never assume the old balance disappeared until you verify it.

What to Do With Monthly Savings

If refinancing lowers your payment, decide in advance how to use the extra money. Without a plan, savings often disappear into everyday spending.

You might build an emergency fund, pay off credit cards, invest for retirement, or make extra principal payments on the new loan. Even modest redirected savings can improve long-term finances.

Lower payments create opportunity when handled intentionally.

Refinancing Is Not the Only Option

Some borrowers need a lower payment but are not ideal refinance candidates. Federal income-driven repayment plans, temporary hardship arrangements, budgeting changes, or increasing income may be better paths.

Private loan borrowers may also ask their lender about temporary relief programs or modified payment options. Not every problem requires a brand-new loan.

Sometimes the best move is restructuring life, not just restructuring debt.

Emotional Relief Matters Too

Debt is mathematical, but it is also emotional. Many borrowers carry shame, frustration, or fatigue around student loans. Lowering payments or simplifying multiple loans into one can reduce stress and create a sense of progress.

That emotional relief should not be dismissed. Feeling more in control often leads to better financial behavior overall.

Money decisions are easier when panic is lower.

Refinancing student loan debt can help lower payments, reduce interest costs, and simplify repayment when done thoughtfully. It tends to work best for borrowers with solid credit, stable income, and private loans or federal loans that no longer need federal protections.

The smartest approach is to compare multiple lenders, understand fixed versus variable rates, choose the right term, and read the fine print carefully. Lower monthly payments are helpful, but only if the overall deal supports your future.

Refinancing is not for everyone, but for the right borrower, it can be a practical step toward financial breathing room and long-term progress.

Found this article interesting? Bookmark it to read again later.

Then, share it for others to read. 🌎

Thank you!

Post Comment