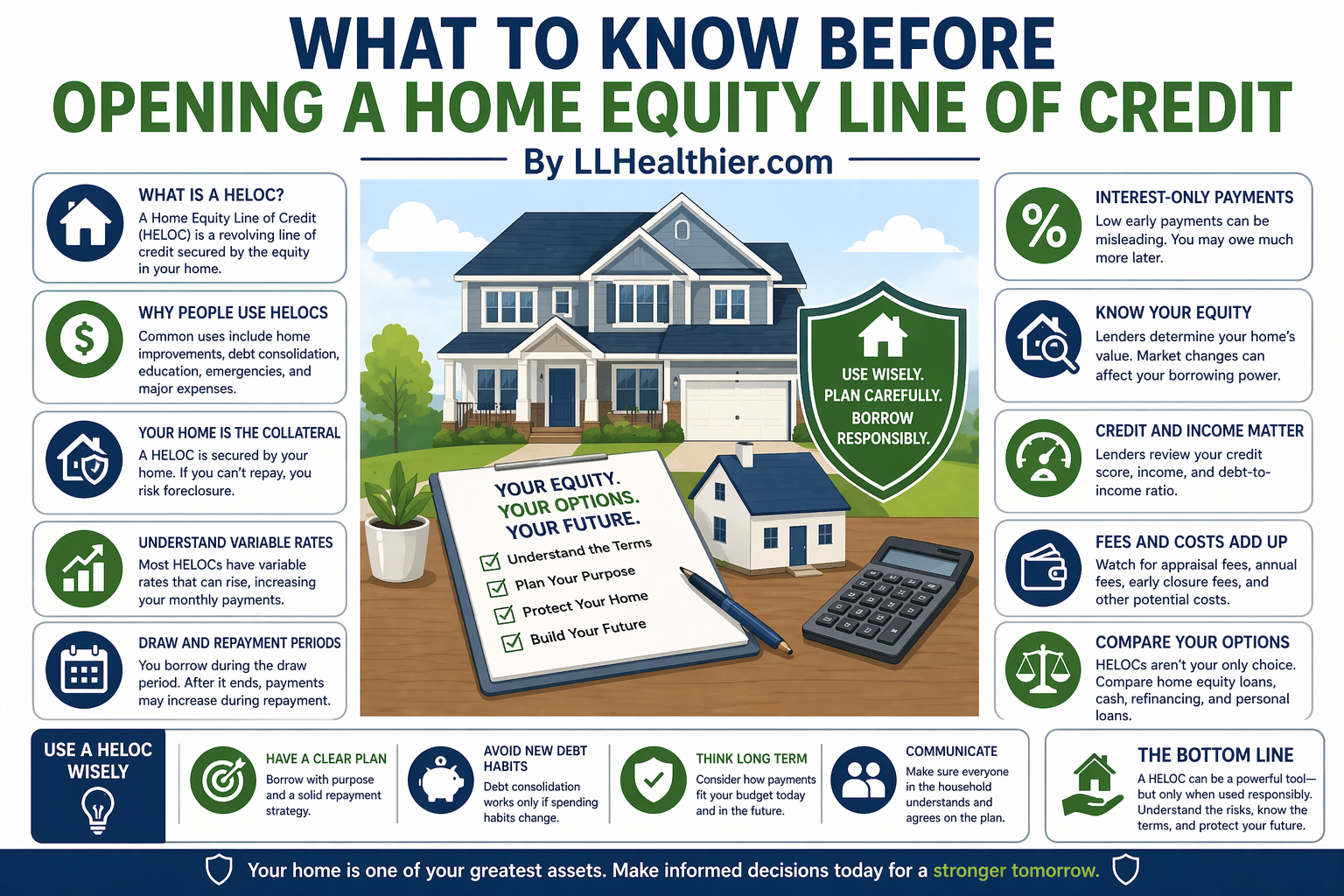

What to Know Before Opening a Home Equity Line of Credit

For many Americans, a home is more than a place to live. It is also one of the largest financial assets they will ever own. As mortgage balances go down and property values rise, homeowners may build equity over time. That equity can create financial opportunities, including access to a Home Equity Line of BeforeCredit, commonly called a HELOC.

A HELOC can be useful in the right situation. It may help fund home improvements, consolidate higher-interest debt, cover emergency expenses, or provide flexibility during a transition period. At the same time, it is not free money, and it is not without risk.

Because your home is tied to the loan, decisions around a HELOC deserve careful thought. Many people focus only on the credit limit and monthly payment while overlooking interest rate changes, repayment structure, and the possibility of using the line in ways that hurt long-term finances.

A HELOC can be smart, but only when understood clearly.

What Is a HELOC

A HELOC is a revolving line of credit secured by the equity in your home. Equity is generally the difference between your home’s market value and what you still owe on your mortgage.

Unlike a traditional lump-sum loan, a HELOC works more like a credit line. You may be approved for a maximum amount, then borrow from it as needed during a set draw period. You usually do not have to take the full amount at once.

This flexibility is one reason many homeowners find HELOCs appealing.

You borrow what you need, when you need it, within approved limits.

Why People Open HELOCs

Homeowners use HELOCs for many reasons. Some use them for kitchen remodels, roof replacement, HVAC systems, or other upgrades that may improve comfort or property value.

Others use them to pay off high-interest credit cards, fund college expenses, bridge temporary cash flow gaps, or manage business opportunities.

Some uses are wiser than others.

Using home-secured debt to improve the home or eliminate expensive debt can be very different from using it for vacations, lifestyle spending, or recurring monthly shortfalls.

Intent matters.

Your Home Is the Collateral

This point should never be minimized.

A HELOC is secured by your house. If payments become unmanageable and serious default occurs, the lender may have legal remedies tied to the property.

That does not mean disaster is around every corner. Many borrowers use HELOCs responsibly and repay them without issue. It does mean the stakes are higher than with unsecured borrowing.

Treating a HELOC casually because it feels convenient can become costly later.

Understand Variable Interest Rates

Many HELOCs carry variable interest rates. This means the rate can rise or fall over time based on market conditions and the lender’s terms.

When rates rise, monthly payments may increase. A payment that felt manageable at one rate can become uncomfortable later.

This is one of the most common surprises for borrowers.

Before opening a HELOC, ask yourself whether the payment would still fit your budget if rates increased meaningfully.

Planning only for best-case scenarios is risky.

The Draw Period and Repayment Period

Most HELOCs have two broad phases.

The first is often called the draw period. During this time, you may borrow funds up to your limit, repay some balances, and borrow again depending on the terms.

The second is the repayment period. Once the draw period ends, borrowing typically stops and repayment begins under a new structure.

Some borrowers are shocked when payments rise during repayment because interest-only payments or lower draw-period payments are replaced by principal-and-interest obligations.

Read this section of the agreement carefully.

Interest-Only Payments Can Be Misleading

Some HELOCs allow interest-only payments during the draw phase.

This can create a lower monthly payment early on, which feels attractive. But lower payments do not mean the debt is disappearing quickly.

If principal is not being reduced meaningfully, the balance can remain largely intact for years.

Later, when repayment begins, the payment may jump significantly.

A manageable payment today should not blind you to tomorrow’s obligations.

Know How Much Equity You Truly Have

Homeowners sometimes assume their home value is whatever they hope it is.

Lenders typically rely on appraisals, automated valuation models, or other underwriting methods to estimate current value. That number may differ from online estimates or neighborhood rumors.

If values decline, borrowing capacity may shrink.

It is wise to be conservative when thinking about equity. Paper wealth can change faster than many people realize.

Credit Score and Income Still Matter

Owning a home does not automatically guarantee HELOC approval.

Lenders usually review credit history, debt-to-income ratio, employment or income stability, existing mortgage obligations, and overall financial profile.

A person with substantial equity but weak income or damaged credit may face limited options, higher costs, or denial.

This is why improving credit and reducing other debt before applying can sometimes strengthen terms.

Preparation can save money.

Fees and Closing Costs Exist

Some HELOCs are advertised with low upfront costs, while others may include appraisal fees, annual fees, inactivity fees, early closure fees, or other charges.

Even when a lender markets “no closing costs,” there may be conditions tied to keeping the account open for a certain period.

Read the fine print carefully.

A HELOC should be evaluated on total cost, not only headline rate or promotional messaging.

When a HELOC Can Be a Smart Tool

Used thoughtfully, a HELOC can solve real problems.

Funding necessary home repairs may protect property value and prevent larger future expenses. Consolidating very high-interest debt into a disciplined repayment plan can sometimes reduce total interest cost.

A HELOC may also provide strategic liquidity for homeowners with strong income and clear repayment plans.

The common thread is intentional use with a realistic exit strategy.

Borrowing works best when there is purpose, structure, and control.

When a HELOC Can Become Dangerous

A HELOC becomes riskier when it supports habits rather than goals.

Using home equity to cover recurring overspending, vacations, luxury purchases, speculative investing, or constant monthly deficits can create long-term damage.

People sometimes feel wealthier because they have equity access. In reality, borrowing against equity is not the same as creating wealth.

If spending behavior remains unchanged, the debt may grow while the underlying problem remains.

Convenient credit can hide financial stress temporarily.

Beware of Debt Consolidation Without Behavior Change

Many people use HELOCs to pay off credit cards.

This can make sense if the new rate is lower and the borrower has a disciplined payoff plan. But if the cards are then run back up, the household may end up with both HELOC debt and new credit card balances.

That is one of the most common debt traps.

Debt consolidation works best when spending habits change at the same time.

Otherwise, it is often just debt relocation.

Consider the Effect on Retirement Years

Older homeowners sometimes open HELOCs assuming they will “figure it out later.”

But income often changes in retirement. A payment manageable during peak earning years may feel heavier later on fixed or reduced income.

Before borrowing, consider where you will be financially five, ten, or fifteen years from now.

Protecting housing stability later in life matters greatly.

Short-term convenience should not create long-term strain.

Emergency Fund vs HELOC

Some homeowners view a HELOC as their emergency fund.

It can serve as a backup source of liquidity in some cases, but it should not always replace cash reserves. Credit lines can be frozen, reduced, or less accessible under certain conditions.

Cash savings provide a different kind of security.

For many households, a balanced plan includes both emergency savings and responsible access to credit rather than relying entirely on one tool.

Compare Alternatives First

Before opening a HELOC, compare other options.

Could you pay cash gradually for the project? Would a fixed-rate home equity loan be more predictable? Could refinancing make sense depending on your current mortgage rate and market rates? Would a personal loan be safer for a smaller need?

Sometimes the best borrowing choice is no borrowing.

Sometimes the best borrowing choice is the one with less risk and clearer terms.

Comparison creates better decisions.

Have a Clear Repayment Plan

One of the healthiest questions to ask before opening a HELOC is simple:

How exactly will this be repaid?

Not vaguely. Specifically.

Will it be repaid through monthly surplus income, bonus income, sale of another asset, a temporary bridge event, or a structured multi-year plan?

If there is no clear repayment path, caution is wise.

Borrowing without a realistic payoff strategy often leads to prolonged stress.

Protect Your Marriage and Household Communication

Money tension can strain relationships.

If you share finances with a spouse or partner, both people should understand why the HELOC is being opened, how funds will be used, what payments may look like, and what risks exist.

Secrets, assumptions, or unclear expectations create conflict quickly.

Shared debt decisions deserve shared clarity.

Read the Terms Carefully

Many financial problems come from documents people never fully understood.

Know the rate formula, margin, adjustment caps, if any, repayment terms, fees, minimum draw requirements, annual fees, inactivity penalties, and conditions under which the lender may change terms.

Ask questions until the answers are clear.

A calm ten-minute question session today can prevent years of frustration later.

Emotional Discipline Matters

A HELOC increases access to money.

For disciplined households, that may be useful. For impulsive households, it may become tempting.

If available credit tends to get used simply because it exists, honesty is important.

The best financial product for one family may be harmful for another depending on habits and self-control.

A Home Equity Line of Credit can be a flexible and valuable tool when used wisely. It can fund meaningful projects, reduce expensive debt, or provide strategic liquidity.

But it is still debt tied to your home. Variable rates, payment changes, fees, and misuse can create serious problems if not understood.

Before opening a HELOC, know your purpose, know the terms, know your repayment plan, and know your own financial habits.

Smart borrowing is not about how much you can access. It is about whether the decision strengthens your future rather than weakening it.

Found this article interesting? Bookmark it to read again later.

Then, share it for others to read. 🌎

Thank you!

Post Comment